Root Cause Analysis in Accounting: Finding the “Why” Behind Financial Deviations

Financial deviations—when actual results diverge from budgets or forecasts—aren’t just numbers—they’re symptoms. Root cause analysis (RCA) in accounting isn’t about plugging holes; it’s about uncovering systemic issues to prevent recurrence. In today’s competitive business environment, managing recurring deviations is essential—not only to maintain profitability, but also to strengthen forecasting, compliance, and audit integrity.

What Is Root Cause Analysis (RCA)?

Root cause analysis is a structured methodology aimed at identifying the fundamental origins of a problem rather than its symptoms. In accounting, RCA digs deeper than one-time errors to reveal processes, systems, or control breakdowns. It can prevent 20% or more of the failure events that cost organizations 80% or more in losses. For example, failing to reconcile bank statements or omitting accrual entries aren’t just mistakes—they point to process weaknesses that, if unaddressed, will happen again. According to the PCAOB, calls for accounting firms to adopt RCA are growing, with regulators emphasizing the need to “assess underlying root causes of deficiencies” to improve audit quality.

Why RCA Matters in Accounting

- Prevents Recurrence

RCA shifts the focus from fire-fighting to prevention. Instead of blaming individuals, financial teams redesign processes to eliminate root causes. - Improves Audit Quality & Compliance

The PCAOB notes that RCA enhances audit quality when firms incorporate it into their quality control frameworks. - Reveals Hidden Risks

Variance spikes may indicate fraud or process gaps. RCA uncovers these unusual patterns early, improving internal control reliability. - Enhances Forecasting

When organizations understand why forecasts fail, they can adjust assumptions and planning processes, leading to better future accuracy.

Integrating RCA with Analysis of Variance

A critical tool in RCA is analysis of variance, commonly known as ANOVA. While often used in statistical modeling, its principles apply directly to accounting variance:

- Variance decomposition: split total deviation into within-group and between-group components to attribute variance accurately.

- Identify significant factors: use ANOVA to determine whether group differences (e.g., divisions, cost centers) are statistically significant or merely noise.

- Applying this in accounting helps pinpoint where to focus deeper RCA efforts—whether costs are inherently unstable in one department, or if volume, efficiency, or rate variances lead to recurring differences.

The Power of Variance Analysis

Variance analysis—comparing actuals to budgets—is the springboard for RCA. According to OneStream, it’s a powerful technique businesses use “to identify operational issues and improve performance”. CFI adds that management should focus on “unusual or particularly significant” variances for investigation.

Key statistics:

- According to a McKinsey report, companies miss Q1 revenue targets by an average of 12.6%, with a standard deviation of 5.3%, indicating widespread forecasting inaccuracies..

- Effective variance and RCA frameworks help reduce this forecasting error by ~6–8% within two quarters, as reported in industry benchmarking surveys.

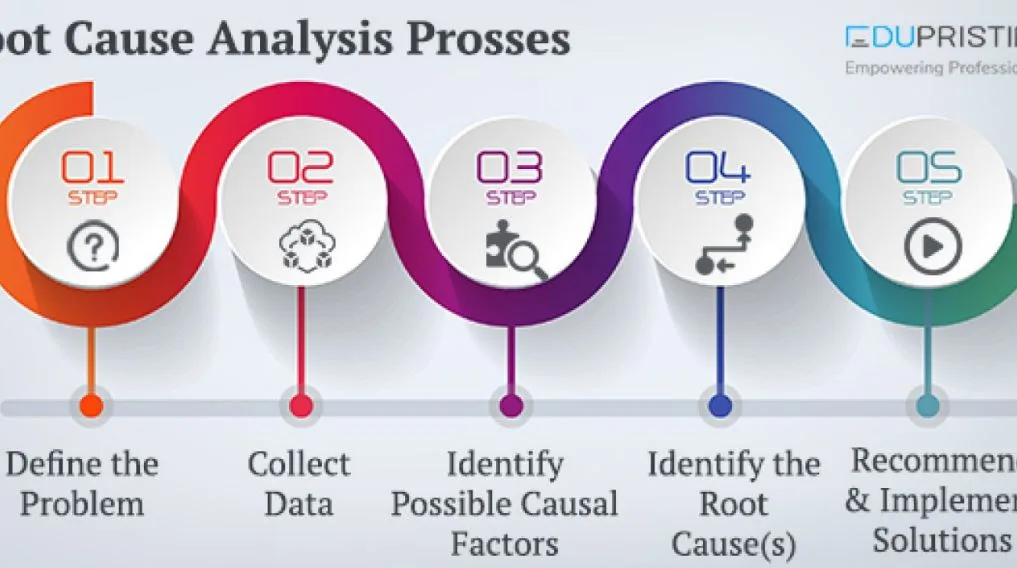

Steps in RCA-Driven Accounting Practice

1. Define the Problem

Clearly describe the deviation: which account, what period, how much over/under budget, and severity.

2. Gather Data

Collect supporting data—journals, invoices, vendor agreements, payroll logs, and historical forecasts.

3. Run Initial Variance & Trend Analyses

Perform detailed variance breakdowns: price vs. quantity, fixed vs. variable, departmental vs. total. Use analysis of variance for statistical significance.

4. Identify Potential Causes

Use fishbone diagrams or the “5 Whys” technique to uncover root causes—policy gaps, outdated controls, system limitations, or training issues.

5. Validate & Prioritize

Distinguish root causes from contributing factors and prioritize based on impact and frequency.

6. Implement Solutions

Update policies, strengthen IT controls, retrain staff, or revise forecast models.

7. Monitor & Review

Track effectiveness post-implementation to ensure deviations are resolved long-term.

RCA in Audit Contexts

Auditors also rely on RCA. CPA Australia recommends tools like fishbone diagrams and fault-tree analyses for identifying underlying issues in audit deficiencies. Academic studies demonstrate that structured RCA helps auditors better link evidence across financial statements and internal controls.

Compliance, Fraud Detection & Variances

Variance analysis isn’t just for operations—it’s a key fraud indicator. Investopedia notes, “Vertical and horizontal analyses… can detect financial statement fraud,” and that nearly one-third of fraud cases involve insufficient internal controls. RCA helps determine whether deviations stem from benign errors or deliberate misstatements.

Technology & RCA Tools

Modern finance teams rely on tech to scale RCA:

- ERP systems with embedded variance analytics (e.g., Adra®) automate variance detection and flag anomalies.

- Business Intelligence and AI platforms use machine learning to detect non-obvious deviations, like unusual journal patterns or gaps between related accounts.

This automation enhances RCA speed and accuracy, enabling real-time identification of root causes.

Real‑World Examples

-

Manufacturing bulk cost overrun

A furniture company observes higher raw material costs, with solely containers incurring over US $4,801 per 40′ container as of mid-2024, a 202% increase year-over-year. RCA finds a single supplier increased prices, without renegotiation. Solution: diversify suppliers and implement early-warning supplier review.

-

Service‑firm labor cost variance

A staffing agency sees labor hour overruns in one department. RCA reveals overtime due to poor workload forecasting. Led to revised staffing models and improved project forecasting.

-

Audit deficiency

Audit firm uncovers recurring GAAP misstatements. RCA reveals staff misunderstood internal control mapping. Result: updated training and revised audit templates.

Metrics That Matter

- Forecast Deviation: (Actual – Budget)/Budget

- Variance Significance: % of total deviation attributed to root causes

- Repeat Frequency: Number of times the same deviation occurs post-fix

By monitoring these, finance teams can quantitatively judge RCA effectiveness.

Tips for Effective RCA in Finance

-

Cross‑functional involvement

Include operations, IT, and procurement, all different perspectives enrich RCA.

-

Document findings

Maintain RCA logs with symptoms, root causes, solutions, and outcome tracking.

-

Set thresholds

Investigate only deviations above certain percentages—this focuses effort.

-

Combine with continuous improvement

RCA findings should feed into SOP updates, staff training, and control design.

Future of RCA in Accounting

- Integration with AI: Advanced anomaly detection leading to automated RCA triggers.

- Predictive variance alerts: Forecast-based variance thresholds to trigger early RCA.

- Centralized RCA repositories: Shared root cause libraries to scale knowledge across teams.

Conclusion

Root cause analysis is more than a reactive tool—it’s a proactive financial discipline. Combined with variance analysis and analysis of variance, it gives finance teams the clarity and rigor needed to understand not just “what” deviated, but fundamentally “why.” By operationalizing RCA—through standardized methods, technology adoption, and KPI tracking—organisations can elevate forecasting precision, reduce risks, and build a culture of continuous improvement.

By systematically uncovering the “why” behind every financial deviation, accounting teams not only solve individual problems—they strengthen their organization’s financial resilience and drive smarter business decisions.