Flipper AI-Powered Trading Aggregator Review: Crypto Perpetuals, Funding Rates, Liquidations

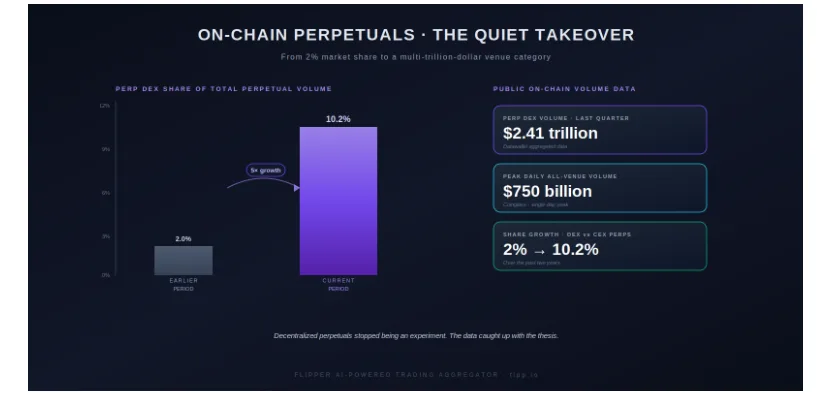

On-chain perpetuals went from roughly 2% of total perpetual trading volume to over 10% in two years. The data is from Datawallet and Coinglass.

Perpetuals are no longer a side experiment on a side platform

Two years ago, decentralized perpetual futures looked like a niche corner of DeFi. Slow execution. Thin books. Most active traders kept the bulk of their leverage on centralized venues and only dipped into on-chain perps for specific reasons. Convenience or yield, mostly. Not core flow.

That picture is now visibly out of date. According to Datawallet’s aggregated data, perpetual DEXs processed roughly $2.41 trillion in combined trading volume across a recent quarter alone. Coinglass has logged daily total perpetual volume peaks approaching $750 billion across all venues. The DEX share of total perpetual trading, which sat near 2% in early 2024, has climbed past 10% on most measurement days, roughly a five-fold increase in market structure terms.

The shift was not a marketing event. Performance caught up. Order books on the leading on-chain venues now clear at latencies measured in hundreds of milliseconds. Liquidation engines handle real stress without socializing losses to other traders. Custody stays with the user instead of with the venue. The reasons traders previously avoided on-chain perps have, one by one, stopped being true.

Which surfaces a different problem. The on-chain perp market is no longer one venue. It is many. Hyperliquid is the largest single source of liquidity. Aster, Lighter, Jupiter on Solana, dYdX, GMX, Vertex, and a long list of others each hold meaningful market share. A position opened on one venue is not necessarily the same trade economically as the equivalent position opened on another, because funding rates, spreads, and book depth vary across them. This is the structural reason a serious perpetuals DEX aggregator becomes useful: not as a UX nicety, but as a way to actually control what a position costs over its lifetime.

Before getting into how aggregation changes the math, it is worth being precise about how a perpetual contract works and where the costs actually live.

What a perpetual contract actually is

A perpetual swap is a derivative contract that tracks the price of an underlying asset, almost always with leverage, and never expires. That last part is the distinguishing feature. Traditional futures have a settlement date. Perps do not. You can hold a long ETH perp indefinitely, in theory, as long as your margin covers the position’s drift against the mark price.

The mechanism that keeps the perp’s traded price close to the underlying spot is the funding rate. Without it, a perp’s price could drift arbitrarily far from spot, since there is no expiration to force convergence. With it, traders on the side that is too crowded pay a small periodic fee to traders on the other side. If longs heavily outnumber shorts, longs pay shorts. If shorts pile in, shorts pay longs. The rate adjusts continuously based on the gap between the perp’s mid-price and the underlying index.

This is the part most retail traders underweight. They think of leverage and they think of the spot price moving. They do not think of the small payment they make or receive every 8 hours. On a $50,000 leveraged position held for two weeks, funding can quietly outpace any spread the trader was worried about at entry. It also varies meaningfully between venues, which we will return to.

The mark price is the second concept worth getting right. When you open a position, the venue uses a mark price (typically an index built from major spot venues) to compute unrealized P&L and to determine your liquidation level. The mark price is not necessarily where your trade last executed. It is the reference price the venue believes is fair. When it moves against you fast, your margin shrinks fast. When it touches your liquidation level, your position closes forcibly, often at a worse price than the mark itself.

The mechanics in one table

| Concept | What it does | Why it matters for your P&L |

|---|---|---|

| Mark price | The reference price used for unrealized P&L and liquidation calculations, usually a weighted index of major spot venues | Mark price drifting against you is what eats margin. Your liquidation level is measured from the entry against the mark, not the last trade |

| Funding rate | Periodic payment between longs and shorts that pulls the perp price toward the underlying spot. Settled typically every 8 hours | Can flip from a tiny positive to an aggressive negative number during volatility. Hidden cost on any position held more than a few hours |

| Open interest | Total notional value of all open positions on a given venue and asset | Heavily skewed open interest is a leading indicator of cascade risk. When everyone is on the same side, the unwind is brutal |

| Margin mode | Isolated margin caps loss to a single position. Cross margin uses your whole balance as collateral | Isolated is safer for testing. Cross is more capital efficient. Mismatching mode and strategy is one of the most common retail mistakes |

| Liquidation price | The mark price at which your margin no longer covers the loss and the position is closed forcibly | Should always be calculated before opening, not after. Funding payments shift this number against you over time |

How a perpetual position actually gets killed

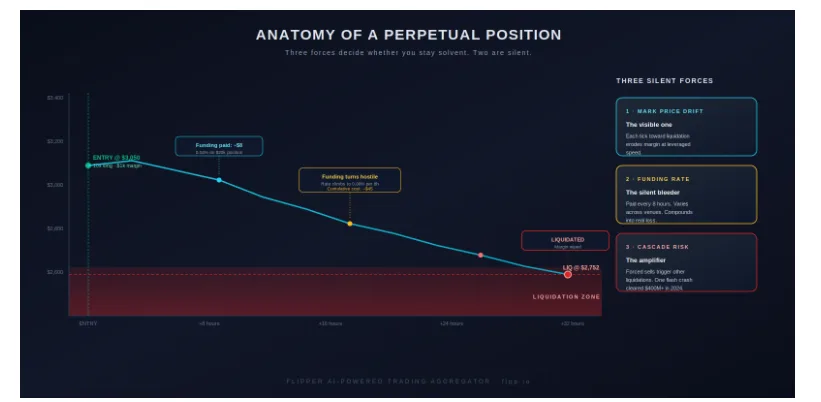

There are two ways a perp position ends badly. The slow way and the fast way.

The slow way is funding bleed. You open a leveraged long during a period when longs are crowded and the funding rate is positive. Every 8 hours, you pay. Maybe 0.01% at first, which feels like nothing. Volatility kicks up. Funding climbs to 0.04%, then 0.09%, then briefly higher. On a $50,000 position, a 0.09% rate per 8 hours works out to roughly 0.27% per day, or about $135 daily. Held for ten days through a hostile funding regime, that is over $1,300 paid before any spot price movement is considered. The trader sees their margin shrink and assumes the trade is going against them. Some of it is. Most of it is funding.

The fast way is liquidation. The mark price moves through your liquidation level, your margin is wiped, and the position closes. On a 10x long opened at $3,050 ETH, the mathematical liquidation level (before fees and funding) sits roughly 10% lower, around $2,745. In practice, funding payments and trading fees nudge that level higher over time. The longer you hold without adding margin, the closer your liquidation creeps to the current mark.

Three silent forces decide what happens to a perp position: mark price drift toward your liquidation level, funding payments compounding in either direction, and cascade risk when many positions share the same liquidation zone.

Cascade risk is the part most retail traders never think about. When a lot of positions are leveraged in the same direction with their liquidation prices clustered, a single price move can trigger forced selling that pushes the price further, which triggers more liquidations, which pushes the price further still. The infamous December 2024 flash crash, in which Bitcoin fell roughly 7% in hours from above $103,000 to under $93,000, liquidated over $400 million in overleveraged positions across centralized and decentralized venues in a single sequence. The trigger was a relatively small spot move. The amplifier was open interest concentration.

There is no aggregator on earth that can prevent a cascade. What aggregation can do is help a trader avoid being the last person in the cascade, by surfacing funding rate signals (rising funding usually precedes crowding), open interest skew, and venue-level health metrics before the position is opened.

The liquidity fragmentation problem in on-chain perps

Here is where the multi-venue reality starts to bite.

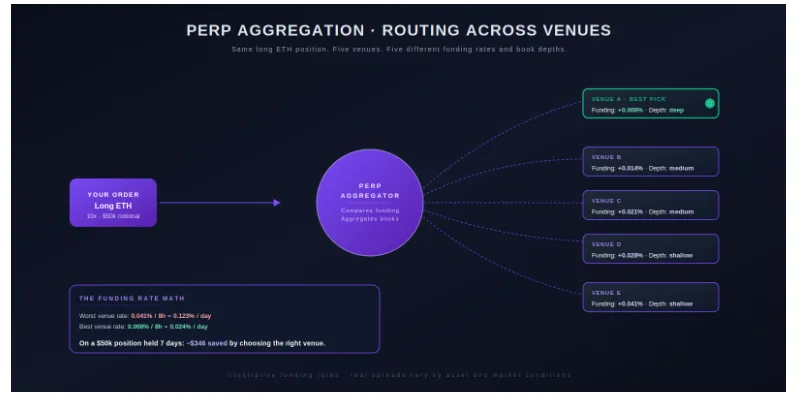

Every perpetual DEX runs its own order book. Every order book has its own depth. Every venue calculates its own funding rate based on its own internal long-short skew, weighted against its own choice of index price. The same long ETH position opened on three different venues can have three different entry prices, three different funding rates, and three different liquidation distances, even when the trader believes they are putting on the same trade.

On low-liquidity pairs or in fast markets, those differences are not small. A funding rate of 0.008% per 8 hours on one venue versus 0.041% on another is not a rounding error. Over a seven-day hold on a $50,000 notional position, that gap works out to roughly $346 in payments avoided just by choosing the right venue, before considering spread or execution quality.

Retail traders almost universally pick a venue based on familiarity, available pairs, or whichever interface they used last time. The decision is essentially random with respect to the actual cost of the position. Sophisticated desks do not work this way. They route. They have to.

What perp aggregation actually does

A perp aggregator solves the same problem in derivatives that a spot aggregator solves in swap routing, with a few additional dimensions. It scans every venue it is connected to, compares funding rates for the asset and direction you are trading, models the spread and book depth at the size you want, and routes accordingly. For larger positions, it can split across venues. For smaller positions, it picks the single best execution path.

The valuable part is not just the entry. It is the ongoing position management. Funding rates change every 8 hours. A position that was optimally placed on Tuesday morning might be 30% more expensive on Wednesday afternoon if funding shifts. A good aggregator surfaces this and either suggests a venue migration or, where the architecture supports it, handles the move transparently.

The same long ETH position priced against five venues. Funding rates and book depths vary widely. The venue with the best combined profile is selected automatically. Illustrative figures.

On top of funding optimization, a well-built perp aggregator brings two other layers that matter for risk-aware traders. The first is venue health monitoring. Not every perp venue is equally robust. Some have weaker liquidation engines, smaller insurance funds, or higher tail risk during stress events. An aggregator that tracks venue health metrics can avoid routing into a venue that is one cascade away from a socialized loss event. The second is non-custodial routing. The trader’s collateral can remain in their own wallet during the entry and exit process, rather than sitting in venue-controlled balances exposed to platform-level risk.

Single-venue manual trading vs. perp aggregation

| Dimension | Trading one perp venue manually | Routing through a perp aggregator |

|---|---|---|

| Funding rate choice | Pay whatever the chosen venue charges, even if a cheaper rate exists elsewhere for the same pair | Best available funding rate selected automatically, recalculated each settlement window |

| Book depth at entry | Limited to the order book of one venue. Larger orders move that single book noticeably | Aggregated depth from multiple venues, order can be sliced across them to minimize impact |

| Spread on entry and exit | Whatever the venue is quoting at that moment, including any temporary widening | Tightest available spread across venues, often meaningfully better on less liquid pairs |

| Risk visibility | Trader manually tracks funding, liquidation distance, and venue health | Aggregated dashboard of position health, funding direction, and venue-level risk signals |

| Custody model | Varies by venue. Some require depositing into a venue-controlled account | Non-custodial throughout, collateral can stay in the user’s wallet during routing |

| Cost over a one-week hold | Funding plus spread plus any unnecessary slippage at entry and exit | Routinely lower by 20 to 40% on common pairs (illustrative, varies by asset and conditions) |

A practical pre-trade checklist for on-chain perps

Whether you are placing a position manually or letting a router do the work, these are the questions worth answering before signing.

- What is the current funding rate on the venue you are about to use, and how does it compare to the other venues offering the same pair?

- What does the order book depth look like at your intended size? A $5k order behaves nothing like a $50k order on a thin book.

- What is the open interest skew on this pair? Heavily one-sided positioning is a warning, not an invitation.

- What is your liquidation price, and how far is it from the current mark in percentage terms? Under 5% is dangerous on any normal-volatility asset.

- Are you using isolated or cross margin? Isolated for tested strategies and experimentation. Cross only when you genuinely understand the cross-portfolio implications.

- How long do you plan to hold? If the answer is more than a day or two, funding cost matters more than entry spread.

- Is the platform you are using non-custodial, or does it require depositing into a venue-controlled balance?

None of these questions require deep expertise to answer. All of them are skipped by the majority of retail perp traders, who tend to focus on entry price and leverage selection and underweight everything that happens after the position is open.

The simple takeaway

Perpetual futures are the largest segment of crypto trading by volume. The on-chain share of that segment has grown by a factor of five over the past two years. The infrastructure has matured. The remaining inefficiency is no longer technical. It is at the routing layer, where the same position can cost meaningfully different amounts depending on which venue absorbs it.

Aggregation does not change what a perpetual contract is. It does not eliminate liquidation risk, funding cost, or cascade dynamics. What it does is move the trader from a position where these forces are invisible into a position where they are surfaced, compared, and optimized at the moment a trade is placed. On a small swing trade, the difference is modest. On a leveraged position held across funding cycles, the difference compounds into real money.

For most traders, the question is no longer whether to trade perps on-chain. The data answered that. The question is whether to trade them on one venue chosen by habit or across the venue landscape with a router doing the work.

See how a non-custodial perpetuals trading aggregator handles routing across multiple venues at flpp.io.