Bi-Weekly vs. Monthly Pay: Which Pay Schedule Is Better for Your Budget?

The Pay Schedule Nobody Warned You About

Your employer decides when you get paid. Most employees accept that without thinking twice. But your pay schedule directly shapes how you manage rent, groceries, debt payments, and savings every single month.

Bi-weekly and monthly pay may deliver the same annual salary, but they create completely different financial rhythms. One gives you more paychecks. The other gives you larger ones. Choose the wrong budgeting approach for your schedule and you run out of money two weeks before your next deposit, even on a good income.

Here is what each schedule actually means for your bank account.

What Bi-Weekly Pay Actually Means

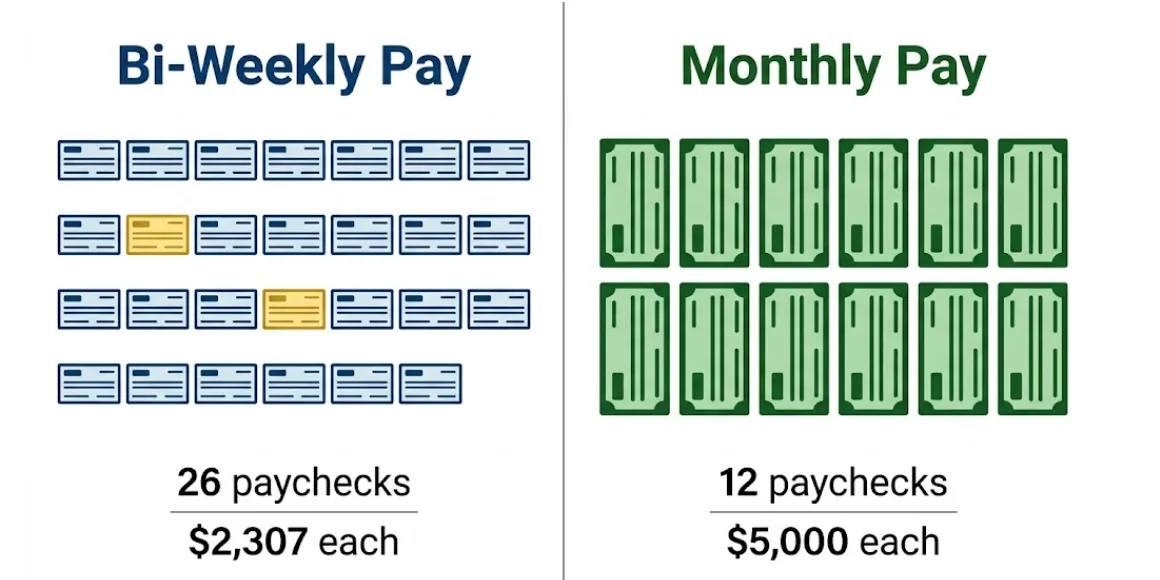

Bi-weekly pay means you receive a paycheck every 14 days, always on the same day of the week. Most employers use Friday. That gives you 26 paychecks per year in a standard year.

According to the Bureau of Labor Statistics, bi-weekly is the most common pay schedule in the United States, used by approximately 43 percent of private businesses.

Each paycheck covers exactly two weeks of work, making the amount consistent and predictable. Your employer calculates federal and state tax withholdings per paycheck using IRS withholding tables, so each check reflects a smaller gross but steadier tax deductions compared to monthly pay.

The key feature of bi-weekly pay is the “three-paycheck month.” Because 26 pay periods do not divide evenly into 12 months, two months each year contain three paydays instead of two. In 2026, those months depend on your employer’s first pay date of the year. If your first paycheck of 2026 falls on January 2, your three-paycheck months are January and July. If it falls on January 9, they land in May and October.

These are not bonus months. Your annual salary stays the same. But those two months give you more cash to work with if you plan ahead.

What Monthly Pay Actually Means

Monthly pay delivers one larger paycheck on a fixed calendar date, usually the last working day of each month or the first. You receive exactly 12 paychecks per year with no variation.

Each paycheck covers a full month of work, which makes the gross amount roughly 2.17 times larger than a single bi-weekly check. On a $60,000 annual salary, your monthly gross is $5,000. Your bi-weekly gross for the same salary is $2,307.69.

Monthly pay is more common in salaried professional roles, government positions, and senior executive jobs. It is less common in retail, hospitality, construction, and healthcare, where bi-weekly is the standard because it accommodates hourly workers and overtime tracking more cleanly under the Fair Labor Standards Act.

The challenge with monthly pay is the long gap between deposits. If rent comes out on the 1st, utilities on the 10th, loan payments on the 15th, and groceries throughout, you are managing 30 days of outflows from one inflow. That requires genuine discipline and a cash buffer that many employees never build.

Bi-Weekly vs. Monthly: A Direct Comparison

Here is how the two schedules compare on a $60,000 annual salary:

| Bi-Weekly | Monthly | |

| Paychecks per year | 26 | 12 |

| Gross per paycheck | $2,307.69 | $5,000.00 |

| Three-paycheck months | 2 per year | None |

| Budget period | 14 days | 30-31 days |

| Tax withholding per check | Lower per period | Higher per period |

| Alignment with weekly bills | Strong | Weaker |

| Overtime tracking ease | High | Lower |

Both schedules produce identical gross annual income. The difference is entirely in timing and how you structure your budget around that timing.

How Bi-Weekly Pay Affects Your Budget

Bi-weekly pay makes weekly expense tracking easier because your budget window is always exactly 14 days. Groceries, gas, and subscriptions fall into a consistent two-week rhythm rather than a shifting monthly cycle.

The predictability helps with cash flow. You know precisely which Friday brings a paycheck, so you can schedule bill payments right after deposits land. This reduces overdraft risk for people who live close to their income.

The main challenge is that your payday rotates through the month. In a standard two-paycheck month, one paycheck might fall on the 3rd and the next on the 17th. In the following month, those dates shift. This means your rent, which is due the 1st every month, does not always align with a pay date the same way twice in a row.

The practical fix is to divide your monthly fixed expenses in half and assign one portion to each paycheck. Rent of $1,400 per month becomes $700 per paycheck in your budget plan, even if you pay it all on the 1st from whichever paycheck lands closest.

If you want to quickly see how your bi-weekly take-home pay translates into annual and monthly equivalents, a salary to hourly calculator gives you an instant breakdown across all pay frequencies, so you can reverse-engineer your budget from any paycheck amount.

How Monthly Pay Affects Your Budget

Monthly pay simplifies the math. Every expense you have is paid from one pool of money that arrives on a known date. Budgeting by month is how most financial tools and apps are designed, so your pay schedule matches the default budgeting format.

The problem is cash flow over 30 days. If your paycheck arrives on the 30th and rent is due on the 1st, you are fine. But if payday is the 30th and a large bill hits on the 15th, you need to hold money for two weeks without spending it, which many people find difficult in practice.

Monthly pay also front-loads financial stress. A large chunk of your paycheck goes to rent, insurance, loan minimums, and utilities in the first week. What remains has to stretch for the other three weeks. People on monthly pay who do not budget proactively often feel rich in week one and cash-poor by week three.

Building a one-month cash buffer, essentially keeping one paycheck’s worth of expenses saved and rolling it forward, solves this problem. But building that buffer takes time and discipline, especially when starting from zero.

The Three-Paycheck Month: Opportunity or Illusion?

Two months per year, bi-weekly employees receive a third paycheck. This is not extra money. Your salary does not increase. It is simply the result of 26 pay periods not dividing evenly into 12 months.

Treating it as a windfall is the most common budgeting mistake bi-weekly earners make. If you spend it freely, you are borrowing from future months, because your normal monthly expenses still apply. Groceries, gas, phone bills, and variable costs do not pause because you received an extra check.

The smart move is to assign that third paycheck before it arrives. Concrete uses include:

Paying down a debt’s principal in a lump sum, which reduces future interest charges. Topping up your emergency fund to cover three to six months of expenses. Front-loading sinking funds for annual expenses like insurance renewals, car registration, or holiday spending. Making an extra mortgage payment, which can cut years off a 30-year loan if done consistently over time.

None of these feel exciting in the moment. All of them improve your financial position measurably by year-end.

Which Schedule Is Better for Paying Bills?

Bi-weekly pay aligns more naturally with recurring weekly costs like fuel, groceries, and childcare. It also makes it easier to make two smaller student loan or credit card payments per month instead of one large one, which reduces average daily balance and therefore interest charges on revolving debt.

Monthly pay aligns better with fixed recurring bills that come on calendar dates, like rent, car payments, and subscription services. When everything arrives and leaves on the same monthly cycle, there are fewer timing mismatches to manage.

If you have significant hourly income, overtime pay, or irregular deductions, bi-weekly pay offers better visibility into each paycheck’s accuracy. You verify two weeks of work against two weeks of pay, which is easier than auditing an entire month in one statement.

Which Schedule Is Better for Saving?

Bi-weekly pay creates 26 saving opportunities per year instead of 12. If you automate a transfer to savings on payday, you save 26 times per year with bi-weekly pay versus 12 times with monthly. Smaller, more frequent deposits are psychologically easier for most people to sustain, and the compounding effect over time is identical to larger monthly deposits.

Monthly pay can work well for savers who prefer a single large transfer, particularly those who max out tax-advantaged accounts like a 401(k) or HSA in one or two deposits per year.

The mathematical savings advantage of bi-weekly pay shows up in mortgage payments. Making one extra mortgage payment per year, which you can fund from a third-paycheck month, reduces the total interest on a 30-year loan significantly. On a $300,000 mortgage at 6.5 percent, one extra annual payment can eliminate roughly four to five years of payments over the life of the loan.

Tax Withholding Differences Between the Two Schedules

Your total annual tax liability is the same regardless of pay frequency. The IRS calculates what you owe based on annual income, not how often you receive it.

What changes is the per-paycheck withholding amount. Bi-weekly paychecks have smaller gross amounts, so each period’s withholding is lower in dollar terms. Monthly paychecks trigger larger per-period withholdings because the IRS withholding tables extrapolate from each paycheck as if it represents a fraction of your annualized income.

The practical effect: your month-to-month take-home varies slightly depending on your schedule, but your year-end refund or balance due reflects your true annual tax situation regardless.

One important note applies to bi-weekly earners. In years with 27 pay periods (which applies to some employers in 2026), the extra paycheck changes per-period withholding slightly. If your employer divides your salary by 27 instead of 26 to calculate each check, your per-period withholding drops, and you may owe slightly more at filing. Check with your payroll department if your employer is running a 27-paycheck year.

If you want to understand how your gross pay converts across all periods, a salary to hourly calculator shows your pay broken down by hour, week, bi-weekly period, and month from a single annual figure, which makes it easier to build a complete picture of your take-home pay before deductions.

State Laws That May Determine Your Pay Schedule

In many states, employees do not get to choose their pay frequency. State labor laws set minimum pay frequency requirements, and employers must comply.

New York requires weekly pay for manual workers. California requires at least semi-monthly pay for most employees. Massachusetts prohibits semi-monthly pay for hourly workers and requires weekly or bi-weekly schedules. Some states, like Alabama, impose no frequency requirements at all.

If you are considering a job that offers monthly pay and you live in a state with minimum frequency laws, verify that the employer’s schedule meets state requirements. Non-compliance can entitle employees to back pay and penalties.

Under the Fair Labor Standards Act, employers who change pay schedules must provide at least 30 days written notice before the change takes effect. If your employer switches you from bi-weekly to monthly without notice, that may violate federal wage law.

How to Budget Effectively on Each Schedule

For bi-weekly earners: Build your monthly budget around two paychecks only. Ignore the third paycheck in your monthly plan and assign it separately when it arrives. Divide all monthly fixed expenses in half and allocate one half to each paycheck. Use a cash buffer of $500 to $1,000 in your checking account to smooth timing gaps between payday and bill due dates.

For monthly earners: Build a one-month cash cushion before anything else. This single change eliminates most cash flow stress on a monthly pay schedule. Pay fixed bills as soon as your paycheck arrives. Separate your variable spending money into a separate account for the rest of the month, so you do not accidentally spend next week’s grocery money today.

Both schedules work well when you match your budgeting method to your pay rhythm rather than forcing a mismatched system onto your income.

Frequently Asked Questions

Is bi-weekly pay better than monthly pay?

Neither is objectively better. Bi-weekly pay suits people who prefer frequent, smaller deposits and those with variable or bill-heavy schedules throughout the month. Monthly pay works better for disciplined savers who prefer managing one large inflow and whose expenses cluster around a fixed calendar date. The best schedule is the one your employer offers, combined with a budgeting system designed for that rhythm.

How many paychecks do you get with bi-weekly pay?

You receive 26 paychecks in a standard year. In some years, including for certain employers in 2026, the calendar alignment creates a 27th pay period. Two months per year will contain three paychecks instead of the usual two.

What is the difference between bi-weekly and semi-monthly pay?

Bi-weekly pay always falls on the same day of the week every 14 days, producing 26 paychecks per year. Semi-monthly pay falls on fixed calendar dates, typically the 1st and 15th or the 16th and last day of the month, producing exactly 24 paychecks per year. Semi-monthly paychecks are slightly larger because the year’s salary is divided by 24 rather than 26.

Does your tax withholding change between bi-weekly and monthly pay?

Your annual tax liability does not change. The per-paycheck withholding amount differs because each paycheck is a different size. On monthly pay, the IRS withholds more per check because each paycheck is larger. On bi-weekly pay, each withholding is smaller. Your year-end tax position is based on total annual income, not frequency.

What should I do with the extra paycheck in a three-paycheck month?

Assign it before it arrives. Strong options include paying down debt principal, fully funding an emergency account, making an extra mortgage payment, or front-loading a sinking fund for a known future expense. Treating it as discretionary spending will not improve your financial position because your regular monthly costs still apply in that month.

Can my employer change my pay schedule?

Yes, but federal law under the Fair Labor Standards Act requires at least 30 days written notice before any pay schedule change takes effect. Some states require longer notice periods. Missouri, for example, requires 30 days advance notice before any wage reduction takes effect. Employers cannot skip a pay period or reduce wages without proper notice and compliance with state law.

How does bi-weekly pay affect mortgage payments?

If you make one extra mortgage payment per year by using a third-paycheck month, you reduce your loan’s principal faster. On a $300,000 mortgage at 6.5 percent over 30 years, making one extra annual payment can reduce the loan term by approximately four to five years. This is one of the most accessible financial strategies available to bi-weekly earners.

Conclusion

Bi-weekly and monthly pay deliver the same annual income. What differs is how that income arrives and how much planning it demands. Bi-weekly pay fits people who want frequent touchpoints with their cash and who benefit from the structured rhythm of a 14-day budget cycle. Monthly pay suits those who can manage a single large deposit across a full month without running dry by week three. Neither schedule is financially superior on its own. What determines the outcome is whether your budget method matches your pay rhythm. Build your spending plan around when money actually arrives, not around the calendar month as a default, and both schedules become workable tools for hitting your financial goals.